The U.S. IRS started accepting 2016 tax returns on the 23rd of January. But many taxpayers are asking “Am I required to file a return?”

The following summary prepared by AG Tax professionals, using the IRS’s guideline, should help you determine whether you are required to file a 2016 tax return or not. In addition, there are situations when, even though you are not required to file, it may be to your advantage to file a return. Some tax situations can be highly complex, therefore, it is recommended to consult a tax professional.

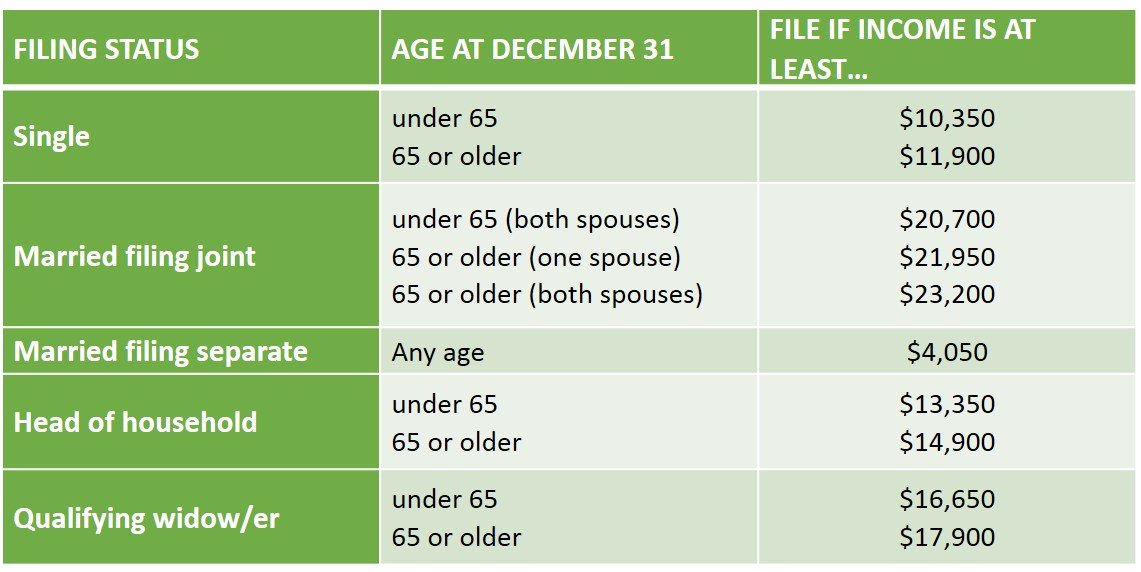

WHEN YOU MUST FILE A TAX RETURN

If you meet the minimum income requirements. The minimum income requirement depends on your age and filing status. The following chart lists the minimum income levels for the various filing statuses:

NOTE: the minimum income level test is based on gross income (before deductions). For example, you must use the gross business income, gross selling price of assets, etc. to determine the income level. It also includes income eligible for the foreign earned income exclusion.

If you are a child or dependent of another taxpayer, special rules apply and a return may be required if income is at least $1,050.

You owe any special taxes

If your income is below the federal income tax brackets, you may still be subject to the Alternative Minimum Tax (AMT). It is important to determine the AMT amount based on the income and deductions that qualify and file the U.S. federal income tax return to report this income.

If you recaptured tax due to claimed education credit and/or first-time homebuyer’s credit, consult your tax advisor for more details.

If you earned income, such as: tips in 2016, which is not reported on Form W-2, and owe social security and Medicare tax on it.

You (or your spouse, if filing jointly) received health savings account, Archer MSA, or Medicare Advantage MSA distributions

If you received an early distribution from a qualified retirement plan (i.e. any withdrawal a 401(k), 403(b), or IRA before age 59½) and are required to pay the early withdrawal tax.

You did not take the required minimum distribution (RMD) from a qualified retirement plan if you are over age 70 (born before July 1, 1942).

You over-contributed more than the allowed limit toward a qualifying retirement plan, such as: an IRA, etc.

You had net earnings from self-employment of at least $400. You will be required to pay the Self Employment tax on these earnings.

You had wages of $108.28 or more from a church or qualified church-controlled organization that is exempt from employer social security and Medicare taxes.

You received advance payments of the premium tax credit for you, your spouse, or a dependent who enrolled in coverage through the Marketplace.

You sold an asset depreciated for tax-purpose at a gain.

You are required to file certain information returns that are attached to a return. This would include Form 5471, Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Form 8865 Return of U.S. Persons With Respect to Certain Foreign Partnerships, Form 8833 Treaty Based Return Disclosures, etc. You are NOT required to file Form 8948 if you are not otherwise required to file a return. Consult your tax advisor for more details.

You are a nonresident alien that earned passive income on which the proper withholding was not remitted. You are also required to file if you have a business within the United States, wish to make an election to include rental property on a net basis or wish to claim treaty exemption from U.S. taxes.

WHEN YOU SHOULD FILE A U.S. FEDERAL INCOME TAX RETURN*

(*even if you are not required to file)

If you are eligible for the Earned Income Tax Credit, Health Coverage Tax Credit, Adoption Tax Credit (on adopting a qualifying child), Additional Child Tax Credit, or American Opportunity Credit; and wish to claim any of these refunds.

You had tax withheld for which you are entitled a refund. This would include a nonresident who had excess tax withheld at source.

You overpaid you estimated tax payments and are eligible for a refund.

If your self-employment income is below $400, you should still file a return to claim any refundable credits for which you may qualify or to carryforward business expense deductions or business losses to the future tax years. It is recommended to consult a tax professional for tax advice specific to one’s personal tax situation.

You wish to establish a loss carryforward. Consult a tax professional to assist you with the tax return filing, and claiming losses in future tax years.

Many taxpayers often assume they do not need to file a tax return. U.S. taxpayers, citizens, residents and non-residents are advised to always file their income tax return on a regular basis if required to do so even in the absence of any taxable income or taxes owing. If you are unsure of your filing requirement, you should consult a professional. In addition, complex issues often require the use of a professional advisor.

Taxpayers should immediately consult their tax advisors to avoid any delay in preparing their tax returns as an accurate and complete tax return could take time. Also, it provides sufficient time to claim possible deductions and credits, which may be overlooked when tax returns are filed in a hurry.

AG TAX LLP CAN HELP

If you have any tax-related queries, need assistance with tax planning or filing your tax returns please contact us. Our team comprises of highly experienced tax professionals with extensive knowledge of US and Canadian tax laws as well as cross-border compliance.

Furthermore, as a full service accounting firm, AG Tax assures complete assistance with even your most complex tax needs.

We can assist with:

- Canadian Personal and corporate tax returns

- Cross Border Taxation and Business Planning

- US Personal and Corporate Taxation

- Disclosure of Foreign Assets and other information filings

- Retirement planning

- Estate Planning, Inheritance tax advice

To obtain a quote or to arrange for a consultation to discuss your tax related queries, please contact us at:

- 604-538-8735 (Greater Vancouver Area, BC)

- 780-702-2732 (Greater Edmonton Area, AB)Disclaimer: The information in this publication is accurate as of the time of its publication. AG Tax assumes no responsibility for changes to tax legislation subsequent to the publication of this document. The information provided is for general information purposes only and should not be acted upon without seeking professional advice. If you would like to engage our services, please contact our staff and obtain authorization to send our firm confidential information. A client relationship is not created by the transmission of information. A client relationship is only formed with our firm when a scope and engagement letter signed by the firm and the potential client detailing the terms of engagement is present.